FinnOne Neo®

FinnOne Neo®Transforming Digital Lending for Your Financial Institutions

Streamlining Transaction Banking for Corporates.

FinnAxia® Global Receivables

Simplify Collections. Strengthen Liquidity. Scale Confidently.

Learn moreTransforming Digital Lending for Your Financial Institutions

Streamlining Transaction Banking for Corporates.

Simplify Collections. Strengthen Liquidity. Scale Confidently.

Learn moreAn advanced technology platform, designed to deliver agile and efficient solutions while drastically reducing the cost of operations.

End-to-end digital lending across the entire lifecycle of origination, servicing & collections.

Learn more

Advanced Automotive Lending Software for complete loan life cycle management.

Learn moreDigital Transaction Banking suite that is modular for a composable banking experience.

FinnAxia®, End-to-end Global Transaction Banking Suite; optimally manages Receivables, Payments, Liquidity, Financial Supply Chains and Corporate Trade.

Learn moreEnsure responsible Lending with our API-backed products for easy & seamless connectivity to the financial ecosystem.

Modern Technology Platform to Engage and Empower Customers.

In this testimonial, Mr. Subodh Rane, Head - BTRG, Retail Assets & Agri, Axis Bank, reflects on a long-standing association with Nucleus Software, spanning nearly two decades of lending ...

In a regulatory environment defined by constant evolution, sustained compliance demands more than periodic alignment - it requires systems that are inherently designed to adapt.In this testimonial,

Welcome to The Orbit Shifting Talks by Nucleus Software - a series where visionary leaders and innovators share insights shaping the future of finance and technology.In this first episod...

In this exclusive interview with Financial IT, Parag Bhise, CEO and Executive Director of Nucleus Software, shares a blueprint for the next wave of innovation in global banking.Discover ...

As financial ecosystems evolve, Nucleus Software continues to lead with purpose and innovation. In this special episode of The CXO Conversations, recorded live at IFF 2025, ...

Innovation. Intelligence. Impact. In an exclusive dialogue hosted by Nucleus Software, Bui Thi Mien, Deputy CRO at MB Bank, reveals how Artificial...

Explore how MB Bank and Nucleus Software's AI-driven digital lending platform FinnOne Neo® are transforming Southeast Asia’s fastest-growing financi...

In this exclusive video, Mr. Chris Taylor, CEO of Deem Finance, offers a firsthand account of the powerful and strategic partnership between Deem Finance and Nucleus...

Artificial Intelligence (AI) is reshaping the lending landscape, offering unparalleled opportunities for efficiency and precision. In this exclusive testimonial, Mr. Pankaj Verma, Head of Credit at M...

Artificial Intelligence (AI) is not about replacing people—it’s about empowering them. As financial institutions embrace digital transformation, AI is emerging as a key enabler of efficiency, decision-making...

Artificial Intelligence (AI) is no longer just an emerging trend - it is becoming mainstream, transforming financial services with automation and data-driven insights. In this exclusive test...

Artificial Intelligence (AI) is rapidly evolving, transforming banking operations and customer engagement at an unprecedented pace. Mr. Narendranath Mishra, Head of Retail & Agri Loans at DCB Ban...

Artificial Intelligence (AI) is driving the next wave of innovation, bringing automation to the forefront of both business and IT operations. In this exclusive testimonial, Mr. Santhi Swaroop Mohanty...

The demand for digitized financial services is growing rapidly, bringing convenience and accessibility to people across regions. Mr. Sourabha Kolhapure, CTO, Mahindra Home Finance,

Mr. Sunil Kapoor, Managing Director of Roha Housing Finance talks about digitizing the mortgage business, his experience with Nucleus F...

Watch Mr. Anirban Ghosh, Chief Risk Officer at Mirae Asset Financial Services, sharing insights into their groundbreaking

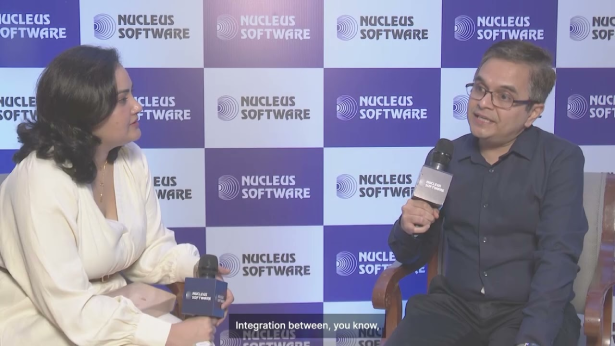

Watch Mr. Amit Bhatia, Head of IT Business Solutions at ICICI Home Finance, share his insights on the seamless integration of FinnOne Neo® with their core banking platform. This ...

How can we help you today?

Lending

Lending

Transaction Banking

Transaction Banking Financial Inclusion

Financial Inclusion