FinnOne Neo®

FinnOne Neo®

Lending

Lending

Transaction Banking

Transaction Banking Financial Inclusion

Financial Inclusion

“Africa is not facing a banking demand problem. It is facing a banking scalability challenge.”

Across the continent, financial inclusion is expanding, digital adoption is accelerating, and customer expectations are evolving at an unprecedented pace. Mobile-first financial services have transformed how customers interact with banks. Regulators are actively promoting digital finance, financial inclusion, real-time payments, and stronger financial ecosystems.

Meanwhile, the African Continental Free Trade Area (AfCFTA) is creating a market of 1.4 billion people with a combined GDP exceeding USD 3 trillion[1], opening new possibilities for regional commerce and cross-border banking.

At the same time, one of the continent’s biggest economic opportunities remains largely untapped.

According to IFC estimates, Africa’s MSME financing gap exceeds USD 330 billion[2]. Small and medium enterprises contribute significantly to employment and economic activity across African markets, yet access to credit remains constrained.

For banks, the opportunity has never been greater.

The challenge is whether their operating models and technology architectures are prepared for the future they are trying to build.

What African Banks Are Asking For?

Over the last few years, I have had the opportunity to engage with banking leaders across Kenya, Nigeria, Ghana, Tanzania, Uganda, South Africa, and several other markets across the continent.

While every market has its own priorities and regulatory landscape, one common theme consistently emerges.

Related Read: From Financial Inclusion to Cross-Border Scale: What’s Changing in Africa’s Lending Landscape?

Banks want to:

- Move faster.

- Launch products faster.

- Approve loans faster.

- Respond to customer needs faster.

- Integrate ecosystem partners faster.

- Adopt AI-driven capabilities faster.

- Scale growth without proportionately increasing complexity.

Yet many institutions find themselves constrained by a reality that is rarely discussed openly.

“Innovation is often moving faster than the core.”

The Challenge Isn’t Always the Core Banking System

For decades, modernization conversations have largely focused on replacing core banking systems. The assumption has been straightforward: if agility is limited, the answer must be a new core.

However, many banks are beginning to discover that replacing the core is not always the fastest path to transformation.

In fact, the challenge is often not the core itself.

The challenge is that too much innovation depends on it.

Over time, customer onboarding, lending workflows, collections processes, product configurations, ecosystem integrations, reporting requirements, and operational decision-making become tightly intertwined with the core banking environment.

As a result, even relatively simple changes can become lengthy projects involving multiple teams, dependencies, and testing cycles.

This creates an important question.

- What if the answer is not replacing the core?

- What if the answer is reducing dependency on it?

Understanding the Concept of “Hollowing the Core”

This is where the concept of “Hollowing the Core” becomes increasingly relevant. Despite its name, hollowing the core is not about removing the core banking system. It is about redefining its role.

The core continues to perform what it was originally designed to do exceptionally well:

- Financial accounting.

- Transaction processing.

- Customer records management.

- Regulatory and compliance integrity.

Everything else can progressively move into agile, configurable, and innovation-focused layers surrounding the core.

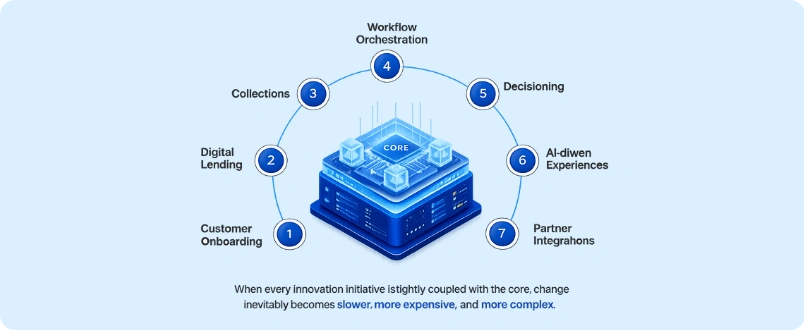

What Moves Outside the Core?

Capabilities such as:

- Customer onboarding

- Digital Lending

- Collections

- Workflow Orchestration

- Decisioning

- AI-driven experiences

- Partner integrations

can operate independently while remaining seamlessly connected to the core. The result is not merely a technology upgrade.

It is a business transformation.

Banks gain the ability to innovate faster without disrupting foundational systems. New products can be launched more rapidly. Regulatory changes can be addressed more efficiently. Ecosystem partnerships can be established more seamlessly. AI capabilities can be integrated without requiring large-scale architectural overhauls.

Why This Matters for Africa’s Banking Sector?

This is particularly relevant for Africa. The continent’s banking sector is simultaneously pursuing multiple objectives.

Banks are expected to:

- Deepen financial inclusion.

- Expand lending

- Support SMEs.

- Enhance customer experience.

- Strengthen governance.

- Improve operational efficiency.

- Embrace emerging technologies.

Achieving all of these goals through traditional transformation approaches can be challenging.

A hollow-core strategy offers a more pragmatic path.

It enables institutions to modernize incrementally rather than through disruptive multi-year replacement programs. It allows banks to preserve investments in existing infrastructure while creating the agility needed to compete in a rapidly changing environment.

AI Is Making Agility More Important Than Ever

The timing could not be more critical. Artificial intelligence is already reshaping how financial institutions think about:

- Credit assessment

- Fraud management

- Customer engagement

- Operations

- Decision-making

Industry estimates suggest that AI can drive productivity improvements of 20-30% across selected banking workflows when implemented effectively[3]

Yet AI thrives in environments that are flexible, connected, and adaptable. The future of banking will not simply depend on who adopts AI first. It will depend on who can operationalize AI most effectively. That requires agility.

Looking Ahead

As African banks prepare for a future defined by digital lending, real-time payments, embedded finance, AI, and greater regional integration, the conversation should evolve beyond technology replacement.

The real question is not whether a bank has the newest core. The real question is whether it can adapt quickly enough to seize the opportunities ahead.

The institutions that lead the next decade may not be those that undertake the largest transformation programs. They may be those that create the greatest agility around the foundations they already have.

Conclusion

In a continent defined by growth, innovation, and opportunity, hollowing the core is no longer just a technology strategy.

It is increasingly becoming a business strategy.